Property Market Support and Common Prosperity: A Contradiction?

Beijing’s latest support measures for the property sector appear to conflict with its common prosperity agenda by disproportionately benefiting high-income groups. This situation underscores a persistent governance challenge for Beijing: balancing immediate economic pressures with long-term ideological commitments.

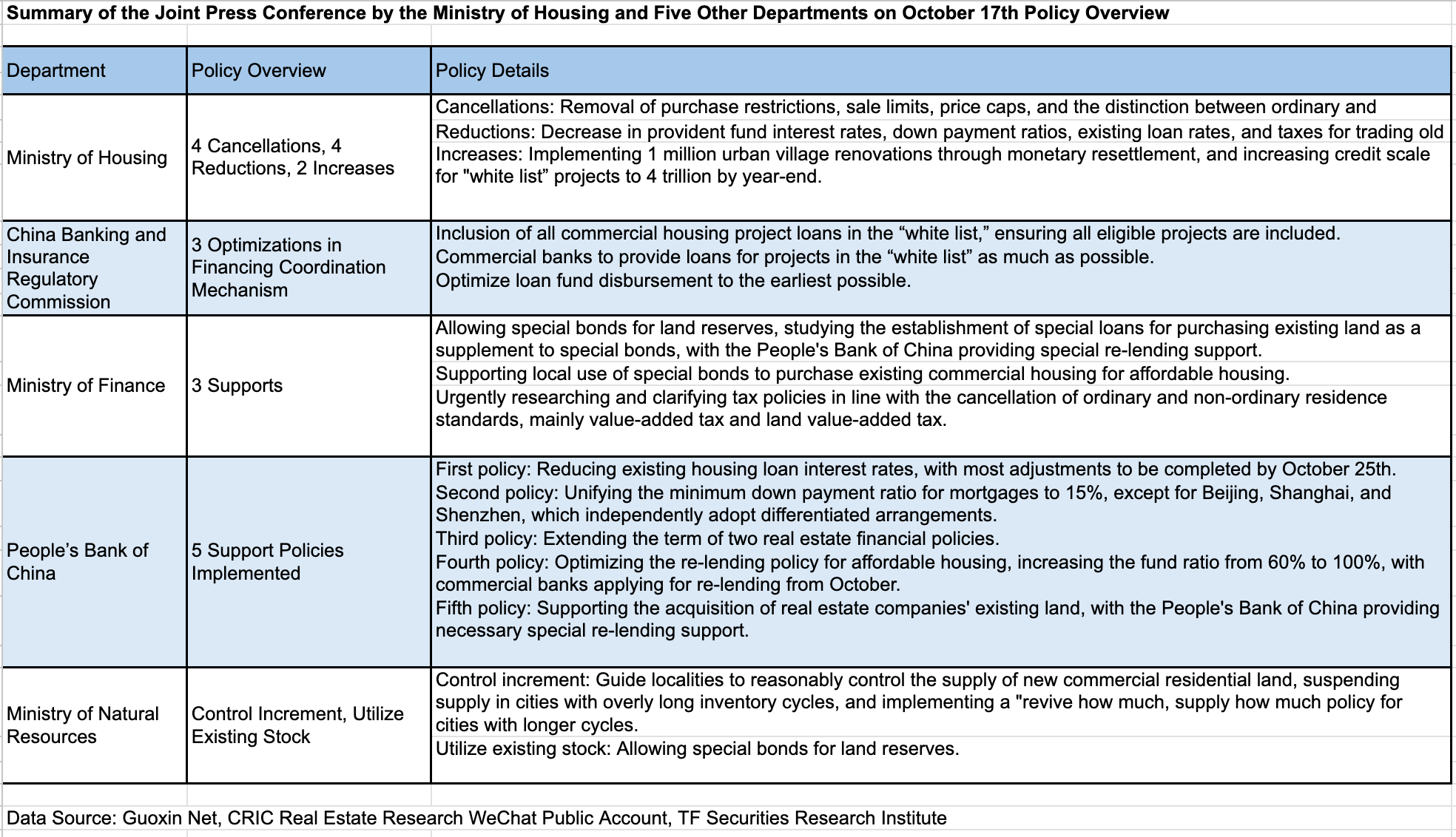

Property Sector Support Measures

Since September, Beijing has announced extensive measures to stabilise the struggling property sector. At a press conference on October 17, Housing Minister Ni Hong, alongside officials from the People’s Bank of China, the Ministry of Finance, and other agencies, framed these interventions as efforts to “stop the decline and restore stability.”

On October 21, the central bank provided additional support by cutting the benchmark loan prime rate for one- and five-year terms by 25 basis points, following earlier rate reductions this year.

These recent measures aim to:

- Stimulate Property Demand and Stabilise Prices: Lowering down payment requirements and easing purchasing restrictions makes real estate more accessible, driving demand and helping stabilise property values.

- Ease Developer Liquidity: Increased financing options and special loans provide developers with essential cash flow, enabling them to clear inventory and maintain operations.

- Restore Buyer Confidence: The policy mandating completed properties before sale assures buyers of project delivery, working to rebuild trust in the market.

- Support Affordable Housing and Urban Renewal: Local governments plan to renovate one million units in urban villages and aging buildings.

Tensions with Long-Term Aspirations

Although these policy measures tackle immediate economic concerns, they may undermine Beijing’s long-term distributive justice goals outlined in the common prosperity agenda. Instead of promoting equitable access to housing and wealth distribution, these policies risk widening the wealth gap by favouring high-income groups.

For instance, lower down payment requirements and relaxed purchasing restrictions mainly benefit wealthy buyers seeking to acquire additional properties. Such measures reinforce an investment-driven market inaccessible to many low-income households facing basic housing challenges.

Moreover, policies designed to support property prices can exacerbate inequality. High property values limit low-income groups from using real estate to accumulate wealth, and as property values rise, those with more property assets experience a disproportionate increase in wealth.

The Role of Property in China’s Wealth Structure

China’s housing privatisation journey began in 1988 and culminated in 1998 with the termination of work unit-based housing allocation and a shift to a market-driven model.

Property ownership now constitutes a significant portion of household wealth, with over 60 percent of household assets tied to real estate—far exceeding the less than 30 percent figure in the United States. By 2023, over 90 percent of Chinese households owned property.

While increasing property values have enabled wealth accumulation for many, they have also created obstacles for new buyers, particularly in major urban centres, exacerbating socio-economic disparities.

Anti-Speculation Policies and the Common Prosperity Agenda

In 2016, Beijing introduced the principle “flats are for living, not for speculation,” aiming to temper property speculation and improve housing access. Policies introduced under this principle include stricter purchasing restrictions, which limit the number of properties individuals can buy, and higher down payment requirements, especially for secondary or investment properties.

This anti-speculative approach aligns with Beijing’s broader equity objectives as outlined in the common prosperity agenda introduced in 2021. The goal is to provide near-equal access to basic public services by 2035 and to expand the middle-income population while significantly reducing income disparities by 2050. The overarching aim is to establish a more balanced development model that fosters socio-economic stability.

However, achieving housing affordability and accessibility remains a formidable challenge, particularly in a growth model where the property sector is a cornerstone of investment and wealth generation.